The economic landscape is currently painted with uncertainty. Recent data reveals a slowdown in Q1 2024 GDP growth, clocking in at 1.6% against a 2.4% forecast, sparking fears of overly restrictive monetary policies. This has led investors to reassess expectations for interest rate cuts. Simultaneously, the April 2024 jobs report showed the weakest gains in new jobs, adding to market volatility. Crude oil prices appear to have peaked, but monitoring supply and demand remains crucial for gauging inflationary pressures.

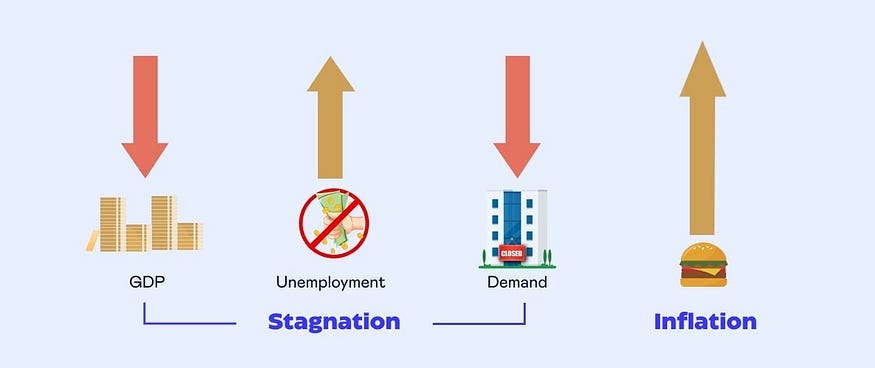

Amidst these concerns, Federal Reserve Chair Jerome Powell offered a dose of optimism during the FOMC press conference, dismissing stagflation fears with the statement, ‘I don’t see the ‘stag’ or the ‘flation’.’ But what exactly is stagflation, and why are these concerns arising? This article delves into these pressing questions, offering insights into navigating today’s complex market.

We’ll examine key economic indicators influencing the Federal Reserve’s monetary policies, analyze crude oil price movements, assess GDP growth, and dissect the latest jobs and unemployment data. Furthermore, we will explore the current inflationary pressures and discuss strategies for investors to navigate these uncertain times. Stay informed and learn how to protect your financial well-being in the face of potential economic headwinds.

Crude Oil Price Trends and Inflationary Impact

Crude oil prices are a critical barometer for the markets, serving as a leading indicator of potential demand contraction. As a primary energy source, oil significantly influences major industries, from agriculture and food prices to the costs of importing and exporting goods. Historically, oil price increases correlate directly with rising prices for goods and services, making it essential to monitor these trends.

Since the beginning of 2024, crude oil prices have been elevated, contributing to inflationary concerns. This upward pressure suggests that interest rates may remain high for an extended period, potentially leading to demand contraction. However, recent CPI and PPI inflation reports have yet to reflect this impact fully. As of early May, crude oil prices have shown signs of stabilization, hovering between $70 and $80 per barrel. Keeping a close watch on price movements from June to September is vital, as the summer months typically bring increased demand due to travel and manufacturing activities.

Interestingly, crude oil prices correlate with the movement of the 10-year US Treasury yield. As yields decline, so does crude oil. The market rally in October 2023 saw oil prices trending downwards, leading the way for a drop in yields. Moreover, increasing oil production in the U.S. could further stabilize prices and ease inflationary pressures by boosting supply, which in turn reduces transportation and manufacturing costs. Given the current election year, there is a strong incentive to maintain stable oil prices to avoid impacting voter sentiment. Expect oil prices to stabilize, potentially leading the way for yields to follow.

Analyzing GDP Growth and Consumer Spending

The first quarter of 2024 revealed a GDP growth rate significantly below expectations. The annualized pace of 1.6% fell short of the estimated 2.4%, raising concerns about the economy’s underlying strength. This, coupled with a notable increase in the consumption price index (3.4% annualized) and a decrease in consumer spending (2.5% vs. 3.3% in Q4 2023), has introduced caution into the market. These factors highlight the importance of vigilance in the current economic climate.

GDP growth is a key metric monitored by the Federal Reserve, as a slowdown can often be attributed to the effects of tightened interest rates. The recent GDP data suggests that monetary policy is working as intended, albeit gradually. The combination of slower growth and higher inflation presents a complex challenge for policymakers.

A closer examination of consumer spending patterns reveals a potential shift in economic behavior. As inflation remains persistent, consumers may be becoming more selective in their purchases, leading to a decrease in overall spending. This shift can have broader implications for economic growth and corporate earnings.

Decoding Jobs and Unemployment Trends

The April 2024 jobs report has raised concerns about the labor market’s health. The Bureau of Labor Statistics (BLS) reported an increase of 175,000 jobs in the U.S. during the month, significantly below market expectations and the slowest gain in six months. Concurrently, the unemployment rate edged up from 3.8% to 3.9%, further signaling potential weakness in the labor market.

The nonfarm payroll data, which captures approximately 80% of U.S. workers, indicates that the ~175,000 jobs added in April represent the slowest gain since October 2023. This figure is also below the 3-month moving average and the pre-pandemic moving average from 2018-2019. These trends suggest a cooling labor market, which could have implications for consumer spending and overall economic growth.

While the markets initially reacted positively to the jobs report, anticipating earlier interest rate cuts by the Fed, the data also suggests a weakening labor market. This could squeeze consumers and put downward pressure on wage growth. Despite potentially decreasing employees’ collective bargaining power, this could lead to a contraction in consumer demand, which, if balanced with the Fed’s dual mandate, could act as a disinflationary force.

Understanding Inflationary Pressures and Market Sentiment

The April CPI data provided some relief, with the headline figure coming in at 3.4% annually (compared to 3.5% previously), and the shelter component (housing and rent) showing decreases (4.5% vs 4.7% previously). According to the Bureau of Labor Statistics, sectors facing abnormal inflation as of March 2024 include auto insurance premiums and shelter. For instance, auto insurance saw a 22.2% year-over-year rise, while rent and housing increased by 5.7% and 4.7% year-over-year, respectively.

It is crucial to recognize that both auto insurance and shelter are lagging indicators, and the effects of monetary policies typically take longer to manifest in these sectors compared to others within the CPI. Auto insurance premiums, for example, are renewed annually, meaning the current increases likely reflect the surge in used and new vehicle prices during the pandemic. Stabilization is expected once these CPI components catch up with reality.

The Federal Reserve’s ability to maintain low unemployment and price stability—its dual mandate—will be critical. The ideal scenario involves effectively combating inflationary pressures without causing significant job losses.

Conclusion: Key Takeaways and Future Implications

The current economic landscape presents a complex mix of challenges and opportunities. While concerns about stagflation linger, a deeper analysis reveals nuanced trends in GDP growth, employment, and inflation. Monitoring crude oil prices and Federal Reserve policies remains crucial for understanding market direction.

The potential for rate cuts, combined with historical trends in election years, offers a glimmer of hope for investors. Identifying companies with strong fundamentals and the ability to refinance debt could yield significant returns as the economic environment evolves.

Ultimately, navigating these uncertain times requires a balanced approach—combining vigilance with optimism and a focus on long-term investment strategies. By staying informed and adapting to changing market conditions, investors can position themselves for success, even in the face of economic headwinds.

Leave a Reply