The 50/30/20 budget rule is one of the most well-known personal finance strategies, praised for its simplicity and ease of implementation. Popularized by Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, this rule suggests allocating 50% of income to needs, 30% to wants, and 20% to savings and debt repayment.

But in today’s economic landscape — where housing costs have skyrocketed, inflation erodes purchasing power, and income inequality is widening — does this rule truly work for everyone? Should a college student, a single parent, or a high-income earner all follow the same allocation?

This article breaks down the strengths and limitations of the 50/30/20 rule and explores how real people have adapted it to fit their financial situations.

Understanding the 50/30/20 Budget Rule

Breakdown of the Rule:

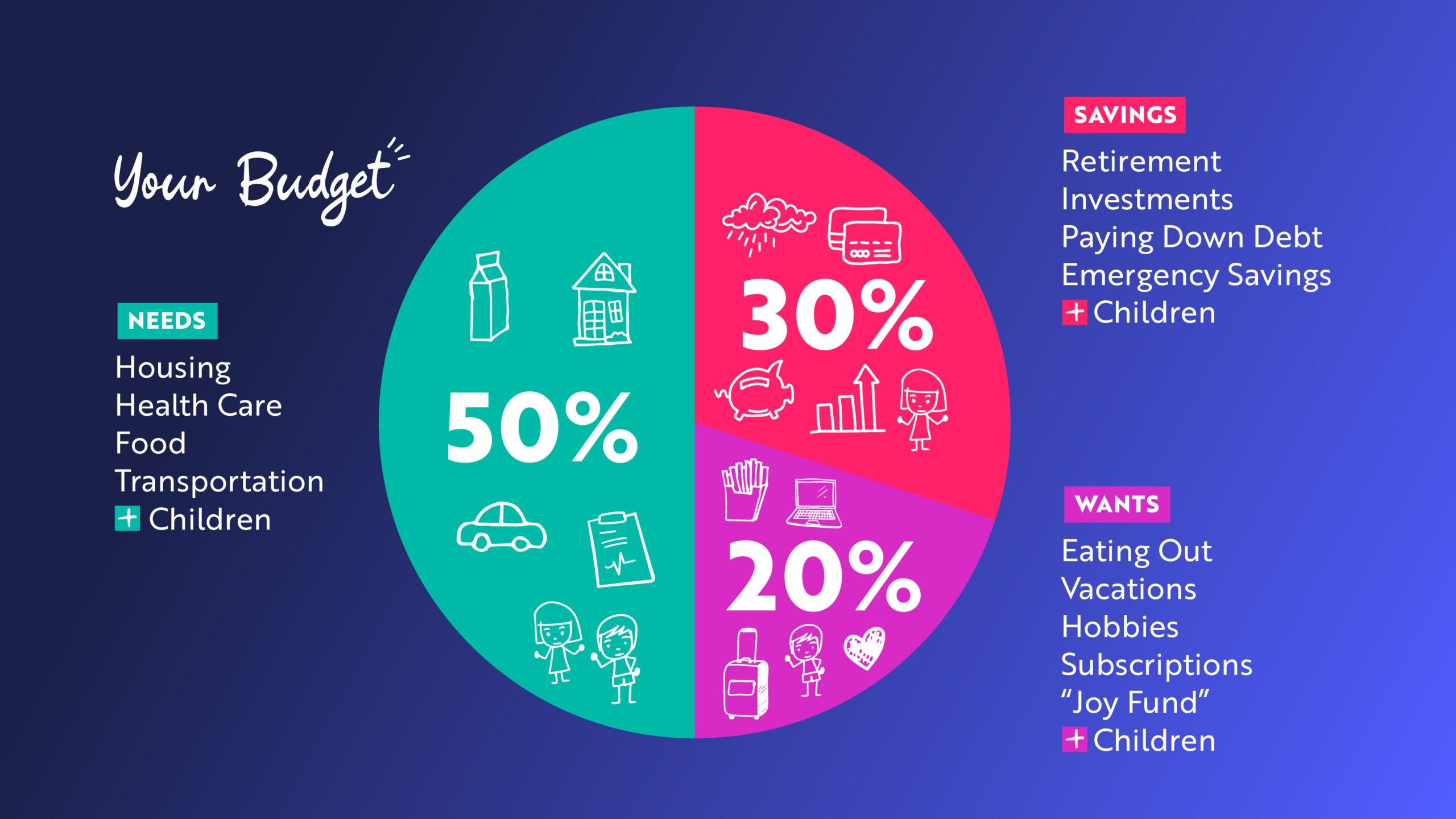

1. 50% — Needs:

• Rent or mortgage

• Utilities (electricity, water, internet)

• Groceries

• Healthcare

• Transportation

• Minimum debt payments

2. 30% — Wants:

• Dining out

• Entertainment (movies, streaming services, hobbies)

• Shopping (clothes, gadgets)

• Travel and leisure

3. 20% — Savings & Debt Repayment:

• Retirement accounts (401(k), IRA)

• Emergency savings

• Extra debt payments (beyond minimums)

• Investments

At first glance, this framework seems practical and balanced. However, financial needs vary widely depending on income, location, and personal circumstances. Let’s look at where this model works well — and where it might fall short.

Does the 50/30/20 Rule Work for Everyone?

1. Low-Income Earner in a High-Cost City

🔹 Case Study: Maria, a Retail Worker in San Francisco

Maria earns $3,500 per month working in retail. She lives in San Francisco, where rent for a small apartment costs $2,200, leaving her with only $1,300 for everything else.

Why 50/30/20 Doesn’t Work for Her:

• Rent alone takes up over 60% of her income.

• Basic groceries and transportation cost her another $600, pushing her “needs” category to 80% of income.

• Saving 20% is impossible without cutting into essentials.

Her Alternative Approach: 70/20/10

• 70% on needs (Rent, food, transport, utilities)

• 20% on wants (Dining out occasionally, entertainment)

• 10% savings (Small emergency fund, paying off debt slowly)

📌 Key Takeaway: If you’re in a high-cost city with a low income, adjusting to a 70/20/10 plan may be more realistic.

2. High-Income Professional Saving for Early Retirement

🔹 Case Study: David, a Software Engineer in Austin

David earns $12,000 per month as a senior software engineer. He rents a $2,500 apartment and lives comfortably, spending about $3,500 on total needs.

Why 50/30/20 Doesn’t Work for Him:

• His needs only take up 30% of his income, leaving extra room for savings.

• He’s planning for early retirement (FIRE movement) and wants to maximize investments.

His Alternative Approach: 40/20/40

• 40% needs ($3,500)

• 20% wants (Vacations, hobbies, gym, dining out)

• 40% savings & investments (401(k), Roth IRA, stocks, rental property)

📌 Key Takeaway: High-income earners should prioritize wealth-building by saving and investing more than 20%.

3. Young Professional with Student Loans

🔹 Case Study: Jessica, an Entry-Level Marketing Associate in Chicago

Jessica earns $4,000 per month and has $800 in student loan payments.

Why 50/30/20 Doesn’t Work for Her:

• Debt repayment is a priority, but it’s categorized under “savings” in 50/30/20.

• Her rent is $1,500, groceries and transport cost $600, and insurance adds $300 — bringing “needs” to 60% of income.

Her Alternative Approach: 60/20/20

• 60% on needs (Rent, food, transportation, insurance, student loans)

• 20% on wants (Concerts, travel, gym membership)

• 20% savings (Emergency fund, extra debt payments)

📌 Key Takeaway: Debt-heavy individuals may need to shift funds from “wants” to debt repayment.

4. Single Parent Managing Child Expenses

🔹 Case Study: Karen, a Teacher in Atlanta

Karen earns $5,000 per month and is a single mother of two.

Why 50/30/20 Doesn’t Work for Her:

• Childcare, education, and medical expenses aren’t luxuries, but they are often categorized under “wants.”

• Extra savings for her children’s future education is a priority.

Her Alternative Approach: 60/25/15

• 60% needs (Housing, childcare, medical, groceries)

• 25% wants (Some fun activities with her kids)

• 15% savings (College fund, emergency fund)

📌 Key Takeaway: Single parents may need to allocate more to needs and education, reducing discretionary spending.

5. Retired Couple Living on Fixed Income

🔹 Case Study: Robert & Linda, Retirees in Florida

Robert and Linda receive $6,000 per month from Social Security, pensions, and retirement accounts.

Why 50/30/20 Doesn’t Work for Them:

• No mortgage (home is paid off), so their needs are less than 50%.

• Healthcare costs and long-term care planning require higher savings.

Their Alternative Approach: 40/30/30

• 40% needs (Healthcare, insurance, living expenses)

• 30% wants (Travel, dining, leisure activities)

• 30% savings (Medical emergency fund, investments)

📌 Key Takeaway: Retirees should focus on healthcare costs and emergency savings rather than strict savings ratios.

Final Thoughts: The Budget Rule is a Starting Point, Not a One-Size-Fits-All

The 50/30/20 rule is a solid foundation for budgeting, but it’s not universally applicable. Your income level, lifestyle, financial goals, and location all play a role in determining the right allocation.

Key Takeaways:

✅ 50/30/20 is a guideline, not a strict rule. Adjust it based on your personal financial situation.

✅ Lower-income individuals may need more for essentials, while high-income earners should save aggressively.

✅ Life stages matter: Young professionals, single parents, and retirees all need different budgets.

✅ Inflation and cost of living should shape your spending allocations.

✅ Flexibility is key: Your budget should evolve with your goals and circumstances.

What’s your experience with the 50/30/20 rule? Have you adjusted it to fit your situation? Share your thoughts below! 🚀

Leave a Reply