I’ll be the first to admit I have a rather unusual, mixed background. A country boy by birth and rearing, and I started learning about the markets due to observing the exceedingly difficult business of running a farm. And by that I mean the pricing of commodities such as the crops grown. Later, in the late 1970s I moved to a city, taking an undergrad in math and computer science. I demonstrated a very strong aptitude for programming, and by the mid 1980s found myself programming in the domain of Artificial Intelligence at AT&T Bell Labs. This gives me an informed perspective about all the hype we’ve been seeing about AI. I’m also a lifelong student of the markets, and am continually struck by the cycles dominating the economy, as well as the prices of stocks, bonds, commodities, whatever. Cycles the greater number of people are ignorant of. And just in case

YOU DOUBT THE EXISTENCE OF CYCLES

in finance, perhaps citing academic theories such as The Efficient Markets Hypothesis (oh boy, where do I start with that one?) let’s look at some examples that are accepted by orthodox economists. First, almost everyone accepts

CAPITALIST ECONOMIES MOVE IN CYCLES

Economic expansion follows recession, just as the interest rates driving the economy fall then rise. But there are other cycles, many many others! In fact I will suggest that

CYCLES ARE ALL AROUND US

The Kitchin inventory cycle was first postulated in 1923 by Joseph Kitchin, a businessman who also engaged in statistics as a hobby. Kitchin postulated inventories across the economy rise and fall in a cycle of between three to five years in length. Because Kitchin wasn’t an academic his work was first ignored, then questioned. Later his research was accepted, and it led to the discovery of other cycles such as The Juglar fixed investment cycle (investments in fixed assets follow a fairly predictable nine to eleven year cycle) discovered by French physician Clement Juglar in 1860, and The Kuznets infrastructue investment cycle (infrastructure investment peaks and falls in a cycle lasting between fifteen to twenty five years in length), postulated by Nobel Laureate Simon Kuznets. There are

LITERALLY DOZENS OF OTHER CYCLES

we are surrounded by. So why would the stock, bond or commodity markets be magically exempt from cycles? Logically they are not and, in fact, cannot be, as markets function within the broader economy. Which is driven by multiple cycles. Oh and the mixed background you ask? Well, I have a strong artistic nature, have made art all my life (it may be crappy art but it is still art!!) and even managed to sell many NFTs of my work during that boom / bust cycle (easy money and some have resold several times). I ran two art galleries in New York’s East Village back in the 1980s, and some forty odd years later still drag my dear wife out to galleries and museums in London on the weekend. It was because of art I first heard the post-modern expression “everything old is new again” applied to the criticism of art or music, the underlying concept being old material is appropriated, then reinvented and reused. Cycles, by another name. Again, cycles are all around us. But what about the stock market? The current

HYPE ABOUT AI REMINDS ME OF THE DOT COM

bubble, or the internet bubble of the late 1990s and early 2000s. This bubble was driven by the growth of and excitement about, the potential of internet based, or dot com companies. Investors were treated to story after story about the potential of the internet to revolutionise businesses and create wealth by doing so. We saw the stock prices and associated metrics of many dot com companies soaring to excessive levels, even though many didn’t have viable business models or were even profitable. Predictions of widespread job losses were common, all due to the power of the internet. Because of the alleged ability of the internet and dot com companies to transform society, many investors and even analysts were willing to overlook the extreme valuation metrics, in favour of ownership of technology stocks at any price. But

A FEW PREDICTIONS DID COME TRUE

such as broad brush descriptions of how some industries would change. Curiously, while many of the original dot com companies went bankrupt, they are generally acknowledged to have laid the foundation for additional advances in technology. In fact, the failure of many of these companies made the business of firms such as Amazon, Google or Facebook possible. I was

WORKING AT DEUTSCHE BANK

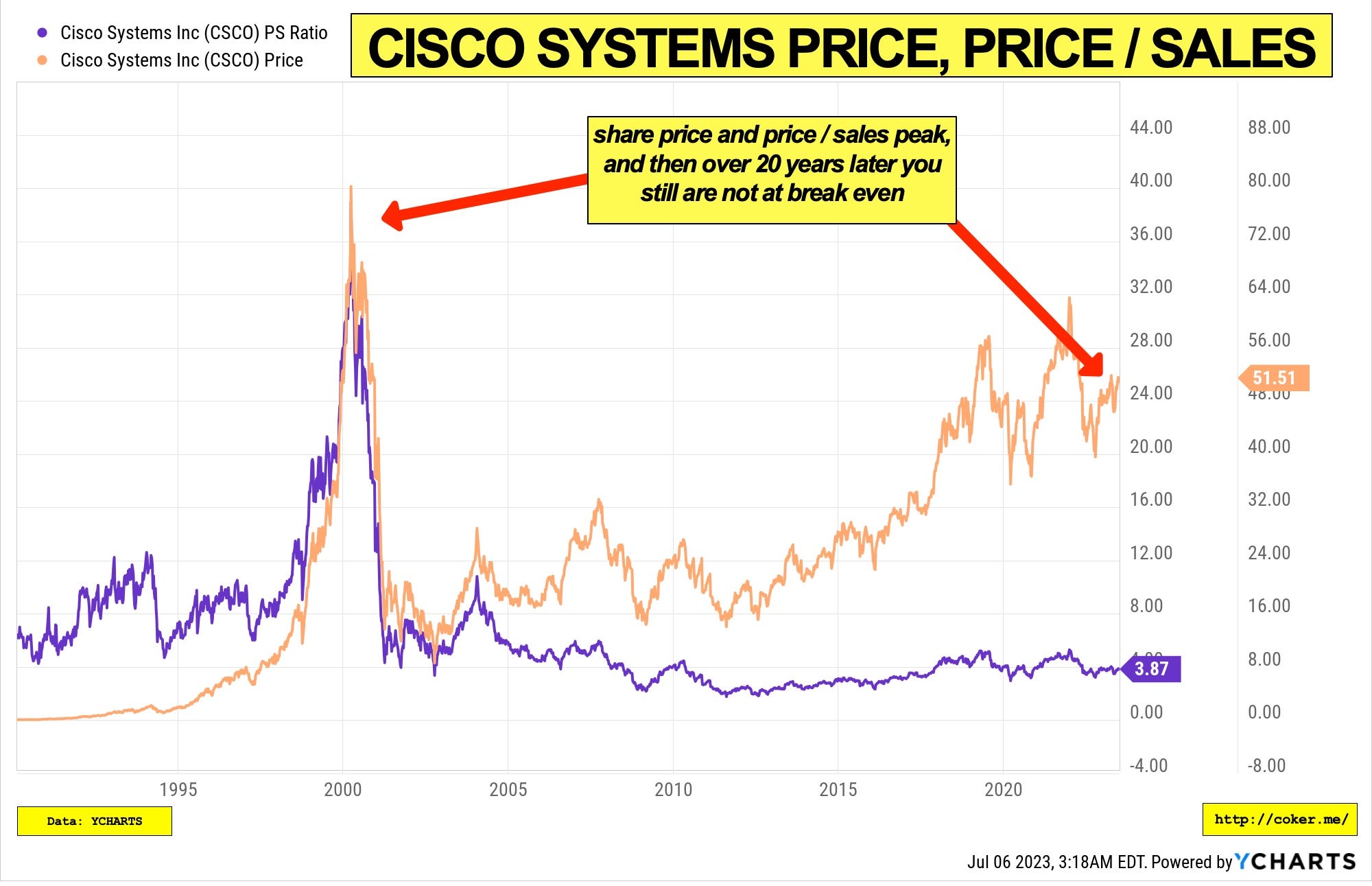

during the dot com bubble times, but paradoxically for someone with a strong technology background, I didn’t own any technology stocks. This was for three reasons. First, the level of hype and predictions, reasonable at the start, seemed to get more extreme as time went on. Second, the extreme valuations and rapid advances in share prices concerned me. And finally, drawn by the modest valuation of REITS (Real Estate Investment Trusts) and their relatively high dividend yields, I started buying heavily in that sector. After all, back then nobody wanted to own dowdy old property businesses, everyone wanted a piece of the next big thing — the internet. A poster child of the dot com era was Cisco systems, a company that sold the networking hardware necessary to make the internet work. Cisco was viewed as the company pushing innovation in internet technology, and driving the entire field forward. Cisco was the company others aspired to be, whether for share valuation or its track record of ground breaking technology. The chart below shows the share price and price to sales ratio for Cisco Systems from July 6th, 1993 to July 6th 2023.

We see Cisco hit a split adjusted high of roughly $77 / share on March 31st, 2000, and the price to sales ratio peaked at 35.01 on April 10th, 2000. We also notice that after the dot com crash, the price of Cisco has never recovered; in other words, if you were unlucky enough to buy Q1 2000 you still haven’t broke even on that trade over 24 years later. And

SPEAKING OF 24 YEARS LATER WE AGAIN FIND

the market distorted by hype, this time about Artificial Intelligence, or AI. I’ve previously written about the poster child for this hype cycle, Nvidia

Where I paraphraised an old Wall Street expression regarding stocks that rise explosively

“If it goes up like a rocket it can fall like a brick”

The chart below shows the share price and price to sales ratio for Nvidia Systems from January 22nd, 1999 to July 6th 2023.

We notice the share price closed July 6th 2023 at $423.17 and the price to sales ratio printed at 40.81, both new highs. Stepping back, it is clear the current hype about AI and elevated prices and valuation ratios (e.g., price to sales) are eerily reminiscent of the dot com bubble. We have it all: bold predictions about massive job losses, forecasts of industries being reshaped and elevated prices for a company perceived as being the driver of technological change. And just

LIKE THE DOT COM BUBBLE

we once again see a cycle of hype and share price overvaluation, repeating itself.

Cycles are all around us.

I hope you enjoyed this article. If you are interested in Financial Independence, Finance, cryptocurrencies and the markets, please considering sponsoring me, at no cost to you, here

all of my content is based on original Market Research I have been selling Investment Banks for years.

Subscribe to DDIntel

Visit our website here:

Join our network here:

Leave a Reply