In my previous article, I discussed an Instagram post by a real estate agent suggesting that saving $578 weekly could lead to a house down payment by year’s end. While feasible, I believe this isn’t the wisest move for most. This article explores better uses for those savings.

You’ve developed a strong saving habit, accumulating an extra $27,744 annually. That’s fantastic! You’ve essentially given yourself a significant raise. But if not for a house, where should this money go?

Pay Off Debt

If your credit score hovers around 700 (remember, the original post mentioned a minimum of 620), that’s commendable! It might be wise to address outstanding debt to push it even higher.

The lower your credit score, the more borrowing money costs, impacting interest rates on cars, college, and homes. Credit card debt is a particularly harmful form of debt, often leading to financial manipulation. Companies often give the illusion that the minimum monthly payment is enough.

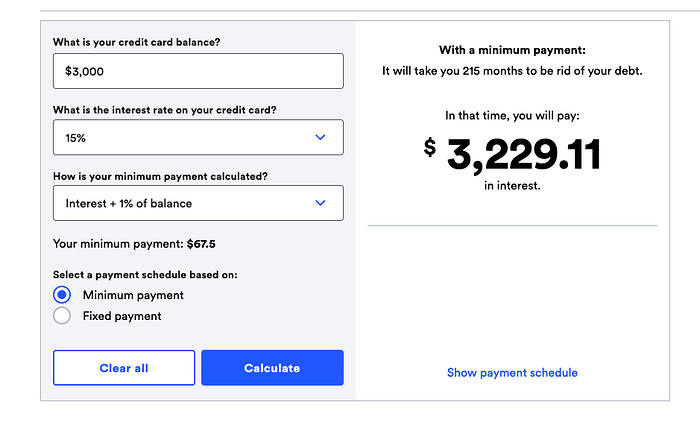

Consider the actual cost of a $3,000 credit card debt with minimum payments of $67.50 monthly.

You’d end up paying almost $3,230 in interest, totaling $6,230 over 215 months (almost 18 years)! Paying just the minimum impacts your credit score too.

If you have a $4,000 credit line and use $3,000, your credit utilization rate is 75%. Experian recommends keeping it below 30%. Using a large portion of your credit implies you’re not conservative, negatively impacting your score.

“In a FICO® Score or score by VantageScore, it is commonly recommended to keep your total credit utilization rate below 30%.” — Experian

Remember that $27,000+ you’re saving? Use it to eliminate credit card debt. Your credit score should improve, leading to lower future interest rates.

High-Interest Savings Account

Another option is to save that money in a savings account for emergencies. To truly grow your emergency fund, consider a high-yield savings account, which offers better interest rates.

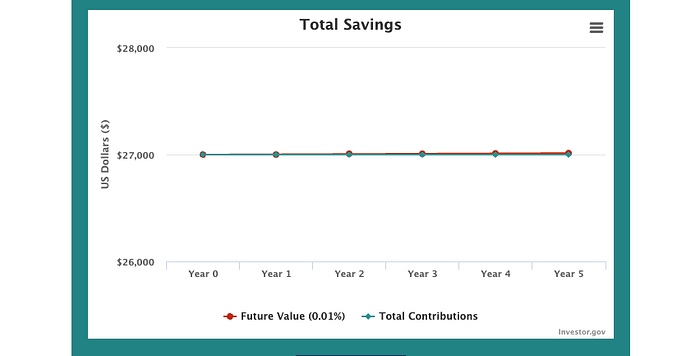

Most banks offer meager interest rates. For example, Chase bank offers a 0.01% interest rate. What does that look like after 5 years?

At 0.01%, $27,000 becomes $27,013.50 after five years. Not much growth.

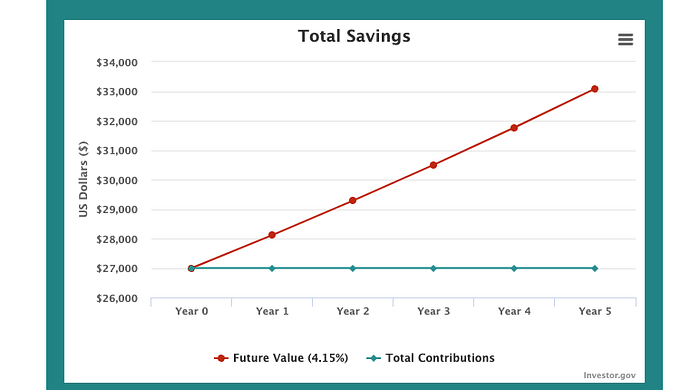

Options exist with rates up to 4.75%. I personally use Marcus, getting 4.15%. Here’s what $27,000 looks like after 5 years at 4.15%.

After 5 years, that $27,000 is now $33,087.21. By simply leaving it in a savings account, I’ve made an extra $5,087.21 in five years—about $1000 per year.

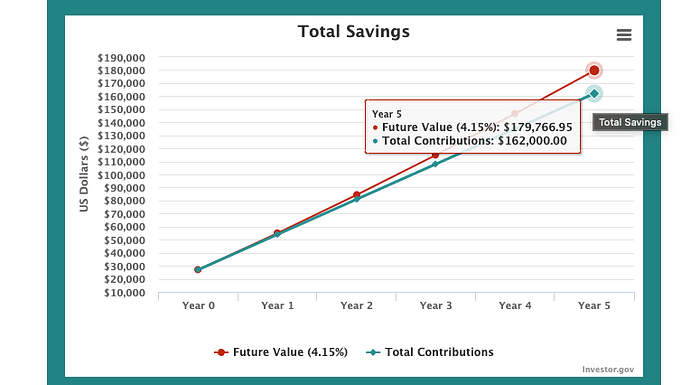

If you consistently save $27,000 a year for those 5 years, contributing $2,250 monthly in addition to the initial $27,000, your savings will look like this:

That’s a growth of $17,766.95 over five years, or $3,553.39 annually. You’d now have almost $180,000 in the bank—a healthy down payment! Even with $50,000 for emergencies, you’d have $130,000 for a robust down payment, earning money on savings instead of throwing it at a potentially burdensome house.

Investing

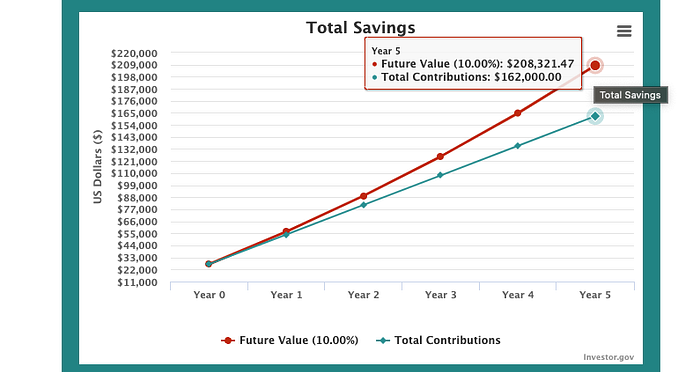

While less immediately liquid, investing can yield better returns. One simple method is opening an individual brokerage account and buying a stock that mirrors the S&P 500 index, such as VOO.

VOO is up almost 311% since 2010, averaging about a 10% ROI annually. Let’s see what our $27,000 looks like with this growth rate after 5 years (with continued monthly deposits).

Having contributed $162,000 over five years, your contributions yield $208,321.47, earning you $46,321.47—an extra $9,264 a year.

Liquidating after 5 years (selling shares and getting cash), you’d have about $199,056.80 after 20% capital gains tax. If keeping $50,000 for emergencies, you now have almost $150,000 for anything you want, including a down payment.

Compound Interest

Compound interest is earning interest on interest. For example:

Earning 10% yearly on $100 gives you $110 at year’s end. In year two, you earn 10% not on the base $100, but on the new base of $110—yielding $11. So after two years you will have $121.

Let’s see what this $100 looks like after 10 years.

After 10 years, your money is 159% higher, not 100%. This compounding effect is most significant when started early.

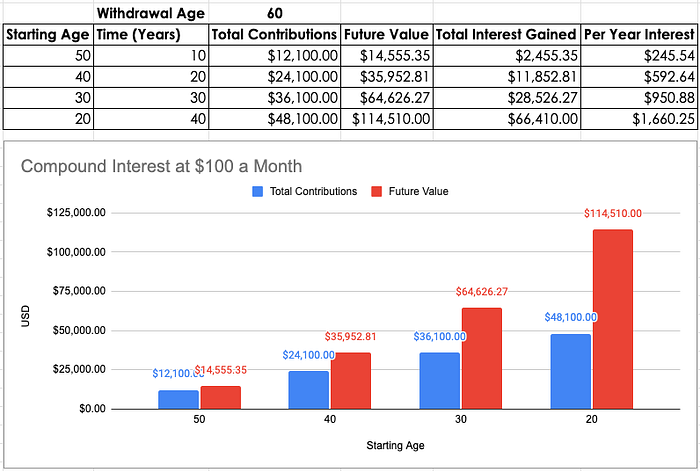

Consider putting $100 monthly into a high-yield savings account at 4% interest, intending to withdraw at 60.

Here’s how much you’d have contributed and received in interest if starting at various ages.

Every 10 years, you deposit $12,100. The earlier you start, the less you need to contribute overall to reach a milestone.

Starting contributions at 50, reaching the $114,510 you get at 60 if starting at 20 requires contributing about $790 per month.

Summary

While achievable, putting $15,000 down if you can’t comfortably afford the $3,353 mortgage and other expenses isn’t ideal.

Reduce spending and maintain good saving habits. These habits will help you contribute to things that actually put more money in your pocket rather than take it out.

Remember, you’ll pay bills living in your home, not receive money.

Your house is only an asset if it provides rental income or if you sell it. Until then, it can be a financial burden if you stretch yourself too thin trying to own it.

Real estate agents receive commission whether or not you can continue to afford the house and live a happy life.

Leave a Reply